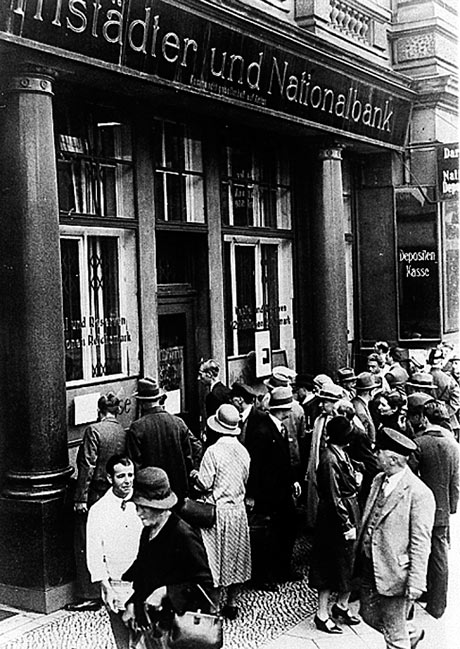

Debt crisis: a crowd gathers at the Darmstaedter and National Bank in Berlin after the bank suspended payments in 1931. Photograph: Associated Press

A country faces an economic and political abyss: the government is on the brink of bankruptcy and pursues fierce austerity policies; public employees take huge pay cuts and taxes are drastically increased; the economy slumps and unemployment rates explode; people fight each other on the street while banks collapse and international capital flees the country. Greece in 2011? No, Germany in 1931.

The government's head is not Lucas Papademos, but Heinrich Brüning. The "hunger-chancellor" cuts government spending by decree, ignoring parliament while GDP falls without limit. Two years later Hitler will be in power, eight years later the second world war will begin. Today's political situation is still different, but the economic parallels are frightening.

Like in today's crisis countries, Germany's key problem in 1931 was foreign debts. The US was Germany's biggest creditor, Germany's debts were denominated in US dollars. Since the mid-1920s, its government had borrowed huge sums abroad to service reparation payments vis-à-vis France and Great Britain. Foreign credit also financed Germany's roaring twenties – the economic boom after the 1923 hyperinflation. Like Spain, Ireland and Greece today, Germany's 1920s upswing was caused by a credit bubble.

The bubble burst when US financial markets collapsed in 1929. US investors and banks were hit hard, lost confidence and reduced their risks – especially their investments in European assets. Credit flows into Germany, Austria and Hungary came to a sudden halt. US investors did not want Reichsmark – Germany's own currency – but dollars, a currency the German Reichsbank could not print. The dollar withdrawal out of Germany – especially out of German bank deposits – led to the quick depletion of the Reichsbank's currency reserves.

To earn dollars Germany had to turn its huge current account deficit into a surplus. But like today's crisis countries, Germany was trapped in a currency system with fixed exchange rates, the gold standard, and could not devalue its currency. However, even upon leaving the gold standard, chancellor Brüning and his economic advisers feared the inflationary effects of a devaluation and a replay of the 1923 hyperinflation.

Without dollar liquidity from abroad, the only way the government could turn around the current account was fierce wage and cost deflation. In just two years Brüning cut public spending by 30%. The chancellor raised taxes and cut wages and social security expenditures in the face of ever increasing unemployment and poverty. Real GNP dropped by 8% in 1931 and by 13% a year later, unemployment increased to 30% and money kept spilling out of the country. The current account turned from a huge deficit into a small surplus.

But there were not enough dollars available on world markets. In 1930 the US Congress had introduced the Smoot-Hawley-tariff to keep imports out of the country. Countries with dollar debts were cut off from the US market and could not earn the necessary money to service their debts. The situation didn't improve when president Hoover proposed a one year moratorium on all of Germany's foreign debt. The moratorium was opposed both by France – which insisted on German reparation payments – and the US Congress. When Congress finally passed the moratorium in December 1931 it was too little, too late.

In the summer of 1931, German banks began to fail, causing both a credit crunch and huge public aid packages to save the biggest banks. The banks had to be closed and the government defaulted on its debts. The Hoover moratorium and a policy of fiscal expansion under Brüning's successor von Papen came too late: bankruptcies and unemployment kept rising and the Nazis gained political ground.

The parallels to today's economic situation are frightening: Greece, Ireland and Portugal have to pursue fierce austerity policies under the pressure of creditor countries and financial markets in order to turn their current account balances from deficit to surplus; Greek unemployment stands at 18%, Ireland's at 14% and Portugal's at 12%, Spain's even at 22%. And those who could help don't do enough: Germany and the German central bankers demand drastic austerity and only give piecemeal and insufficient help in return – too little, too late, now and then.

Much would have been gained for Germany in 1931 if the US – and also France – had provided the necessary liquidity for German banks and its government. Maybe the political radicalisation could have been avoided. But the US was turning isolationist. It did not want to get involved in messy European affairs.

Today Germany plays the US role. Both parliament and the government hesitate to provide the necessary help for the crisis countries: within the EFSF, Germany is willing to guarantee only up to €211bn of crisis country borrowing. This is not enough. The 2008 guarantees for the German banking system were €480bn.

Germany still insists on its current account surpluses. These are, by definition, the deficits of the crisis countries. Thus they keep these countries from earning the money to service their debts. Further, Germany fiercely opposes liquidity credits by the ECB. German economists and central banker justify the ECB's passivity with the threat of inflation. But they mix up the historical lessons from Germany's 1923 hyperinflation and its 1931 deflation and unemployment crisis.

This failure of judgment can easily backfire: Germany's reputation all over Europe is already declining, political tensions in crisis countries with record unemployment are increasing drastically and the ever more likely breakup of the eurozone would threaten Germany's economy, especially its banks and exports.

The US learnt the hard way that it had to take responsibility for the world's economic stability. The second world war was one of the consequences of the 1930s crisis that it could have prevented.

After having failed to stabilise the world economic system in the early 1930s, by 1945 the US had learned that only economic co-operation could lead to a peaceful and prosperous world. Via the Marshall plan and the opening up of its markets for European exports it allowed Europe to rebuild its destroyed economy. Meanwhile, US exporters profited from Europe's hunger for investment and consumption goods.

Until the early 1970s the US led the international trade and currency system – the Bretton Woods system – thereby guaranteeing economic prosperity, a free market with social equity and thus the economic pre-requisites for social democracy.

Both the German public and politicians should learn from history. Solidarity with the crisis countries is in Germany's long-run interest. The German government should stop abusing its power to dictate economic decline to other nations. The alternative is economic stagnation and increased tensions between European nations. The verdict still holds: those who are not willing to learn from history are bound to repeat it.

Δεν υπάρχουν σχόλια:

Δημοσίευση σχολίου